Australian Equities: Year In Review 2024

08 August 2024

Reflecting on the last financial year in Australian equities, our expert partner Northcape Capital, share their views on the key themes driving markets. Notably the team sees a substantial mispricing across sectors consistent with a momentum approach and a focus on near-term earnings revisions. For investors like Northcape who are focused on “quality” companies, the opportunity set is expanding.

This information has been prepared by Northcape Capital, the underlying investment manager for the Warakirri Concentrated Australian Equities Fund and Warakirri Ethical Australian Equities Fund.

Investment Themes Observed in 2024

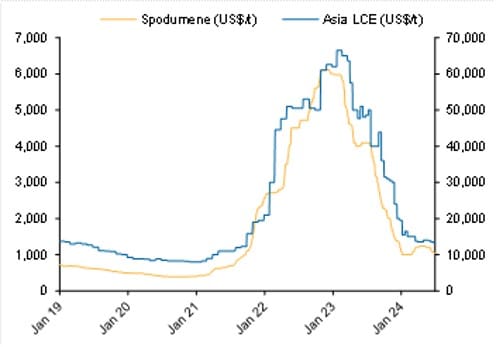

Lithium – A cautionary tale

Lithium stocks have fallen by as much as 60% over the last 12 months and were some of the biggest losers in our market. This time a year ago, lithium prices were 4x higher than their current level today thanks to supply shortages and a seemingly insatiable demand for electric vehicles (EVs). There has since been a reset in EV expectations, as sales growth has slowed in all major markets.

Despite the crash in lithium prices this year, we have barely seen supply come out of the market. In fact, producers such as Pilbara Minerals are now contemplating a further doubling of production capacity by the end of this decade!

Do lithium stocks look cheap now? We remain cautious. Our recent trip to China showed that there is growing supply from lepidolite (a low-grade ore that contains lithium), both from China-based mines and Chinese-owned mines in Africa. These projects have historically been considered much higher cost than those in Australia and South America. However, growth in demand has led to increased scale and efficiency, driving lower unit costs.

The ability of the mining industry to rapidly scale up to meet demand for lithium has caught many observers by surprise. We doubt that prices will fall much further given the outlook for demand growth over the coming decade, but we also suspect the potential long-term upside is limited. Interest in lithium projects is still a relatively new phenomenon and many new deposits and new extraction techniques are currently being explored, which could affect the industry cost curve in future years.

The rapid rise and fall in lithium this past year has shown how hype can build around a theme but also quickly lose steam when the market changes its mind or takes a closer look at the fundamentals. We are seeing clear signs of this elsewhere, including in the artificial intelligence frenzy today. Our disciplined approach towards stock selection has proven itself over the last two decades through many cycles and again proved to be the right approach this past year when it came to lithium.

Exhibit 1: Spodumene and Lithium Carbonate prices have come back down to earth

Source: Bloomberg

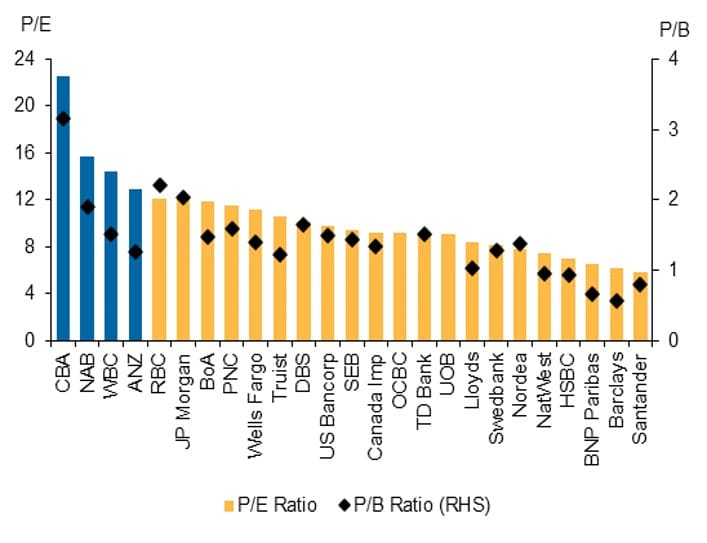

Banks – Momentum over fundamentals

Over the last 12 months the major banks have generated total returns including dividends of 35% on average, outperforming the broader market by 23% and the Materials sector by 38%.

Remarkably, earnings revisions were negative during the year, implying the entire rally was driven by sentiment.

The major banks now trade on a record average one-year forward price-to-earnings multiple of 16x, with CBA on a previously inconceivable multiple of 23x. CBA is by far the most expensive large bank in the world on a range of metrics. Coupled with expectations of only 1% earnings growth each year over the next 4 years, and the lowest dividend yield amongst peers, the risk reward for CBA looks particularly unappealing to us at present.

Intriguingly, no sell-side analyst has a positive fundamental view of the sector, and no analyst or bank executive can explain the rally in fundamental terms. The lack of any debate on the fundamentals hints at flow-based explanations for the rally.

Exhibit 2: Australian banks are the most expensive among global peers

We suspect a combination of regional ETF buying and momentum-based strategies, but the exact explanation is less important than our conviction that the fundamentals will prevail eventually.

Competitive pressures in retail banking remain a key issue facing the banks. Structural changes including the rise of mortgage brokers has driven commoditisation of home loans, with 70% of all new residential home loans being written by brokers rather than by the banks themselves. New digital-only entrants such as Macquarie have disrupted the economics in the home loan market with simple, low-cost offerings.

Higher operating costs and large investment programs also pose risks to bank earnings. Westpac is planning to spend at least $2bn a year for the next 4 years to simplify its complex and outdated technology stack to bring it in line with peers. ANZ is facing higher investment spend in transitioning to its new ANZ Plus platform and risks losing valuable deposit customers in the process. It has further complicated this task by buying Suncorp bank. It remains to be seen who will be accountable for these programs running on time and on budget, with both banks’ CEOs speculated to be leaving within the next year.

Data centre demand: “byte-ing” off more than it can chew?

The potential of generative AI has captured public and market imagination, much like lithium did in the year before. This enthusiasm is evident in the re-rating of companies with data centre assets, such as NEXTDC (NXT) and Goodman Group (GMG), which house servers for AI models. These companies are seen as essential tools in the AI gold rush, expected to experience hyper-growth. However, challenges loom.

AI workloads are power-intensive, requiring 2.5 times more power than non-AI workloads. Global data centre capacity is forecast to more than double in the next four years, but this growth faces significant electricity supply constraints. For instance, a 300 MW data centre, like NXT’s S4 in Sydney, consumes electricity equivalent to 200,000 homes and has a physical footprint of about 100,000 sqm. Supporting such a data centre with renewable energy, like solar power, would need a generation capacity equivalent to the 1.3GW Upper Calliope solar farm, which uses over 27 million sqm of land and costs around $2bn, half the cost of the data centre itself. It would also rely on additional firming power which is increasingly under pressure at the grid level and will eventually have to be provided and paid for.

Some regions, like Singapore, Ireland, and the Netherlands, have already imposed moratoriums on data centre developments due to power supply constraints. Electricity capacity is likely to be a major constraint on AI demand growth, given political and energy transition commitments.

Even without electricity constraints, the surge in proposed large-scale data centre builds risks a demand-supply imbalance, exacerbated by high upfront capital and long payback periods. These long duration assets are sensitive to minor assumption changes, making miscalculations costly. With modest returns even at face value, we find the risk-reward unattractive and prefer to sit on the sidelines.

Instead, we prefer an exposure in BHP as a potential beneficiary, with significant exposure to copper (we estimate ~30-40% of normalised medium-term profits for BHP), a critical element used to conduct electricity (and heat) that is used extensively not only in data centres and power generation and distribution (and hence will also stand to benefit from any sustained AI driven demand) but also from the ongoing electrification of our world, from EVs to wind turbines and solar panels.

Market Outlook and Portfolio Positioning

As the saying goes, “There are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.” We would like to think of ourselves as being in the former, that is we remain cautious about making economic and market forecasts for the year ahead, particularly in light of momentum and sentiment-driven flows having a larger impact on share markets than ever before.

Against this backdrop, we see the Australian stock market as being in a unique predicament now. Despite the cash rate sitting at 12-year highs, the RBA is now facing the prospect of raising rates further this year to put the handbrakes on growth. At the same time, cost-of-living pressures are already weighing heavily on households, and many are struggling to service their ballooning mortgage repayments. It goes without saying that the RBA must walk a fine line between slowing down inflation and ensuring the economy does not grind to a complete halt.

Unemployment remains at historic lows, but this looks to be changing. In May, Telstra announced a reduction to their direct workforce of 2,800 jobs which marks the first post-COVID large scale program of redundancies announced by a major Australian corporate. Other Australian corporates are also facing inflationary pressures, declining labour force productivity (exacerbated by Federal labour law changes) and emerging opportunities for technology driven efficiency to replace human capital. Companies with high operating margins and pricing power should fare relatively better and we continue to align our portfolio with these market leaders.

In our view, the market has not adequately priced in the risk of persistently high and volatile inflation. For example, the equity risk premium in Australia is sitting at around 2% which is near 15-year lows.

In general, we have been selling domestic stocks with consumer discretionary exposures, including JB Hi-Fi, Wesfarmers and Seek. Our bank underweight further tilts us away from the Australian consumer’s woes.

Decarbonisation and energy transition progress has slowed this year as high interest rates have impacted green investment spend and the pathway for transition remains unclear. However, we think Worley and Macquarie remain well placed to help facilitate the global transition to renewables as it takes place.

We entered the financial year with large overweight positions that underperformed the year before but had resilient earnings, such as James Hardie, Fisher and Paykel and ALQ. These names subsequently rallied and have been amongst the best performers in our portfolio this year. As we enter the new financial year, we again see substantial embedded alpha in our overweight positions, including IDP Education, Brambles, Telstra and Transurban. These quality defensives have been left behind in the market’s run-up despite demonstrating improving prospects.

In summary, we see substantial mispricing across sectors consistent with a momentum approach and a focus on near-term earnings revisions. For investors like ourselves focused on quality and long-term value, the opportunity set is expanding. We will always maintain a diversified portfolio whilst exercising patience and discipline to seize favourable opportunities that come our way. We hold a high degree of confidence in the outlook for our portfolio in the year ahead.

For more information, please contact us on 1300 927 254 or visit Our Funds.

The information in this document is published by Warakirri Asset Management Limited ABN 33 057 529 370 (Warakirri) AFSL 246782 and issued by Northcape Capital ABN 53 106 390 247 AFSL 281767 (Northcape) representing the Northcape’s view on a number of economic and market topics as at the date of this report. Any economic and market forecasts presented herein is for informational purposes as at the date of this report. There can be no assurance the forecast can be achieved. Furthermore, the information in this publication should only be used as general information and should not be taken as personal financial, economic, legal, accounting, or tax advice or recommendation as it does not take into account an individual’s objectives, personal financial situation or needs. You should form your own opinion on the information, and whether the information is suitable for your (or your clients) individual needs and aims as an investor. While the information in this publication has been prepared with all reasonable care, Warakirri and Northcape do not accept any responsibility or liability for any errors, omissions or misstatements however caused.

![]()