3 Key Lessons from Two Decades of Managing Australian Equities

29 October 2024

The impact of the decisions we make today often take time to become apparent. Investing is the same; at first you may not see the results but over time the value of good decisions compounds. As our investment partner, Northcape Capital, celebrates 20 years of managing Australian equities, they share three key lessons that have helped form the foundation of their success in the asset class.

This information has been prepared by Northcape Capital, the underlying investment manager for the Warakirri Concentrated Australian Equities Fund and Warakirri Ethical Australian Equities Fund.

The Power of 20 Years of Compound Growth

“Someone is sitting in the shade today because someone planted a tree a long time ago.“ – Warren Buffet.

In life, we often feel the effects of decisions we made years ago. Like planting a tree, the impact of the decisions we make today take time to become apparent. Investing is the same. Initially you may not see significant results but over time the value of good decisions compounds, providing future “shade” in the form of financial security, wealth generation and retirement readiness.

Northcape first “planted its tree” 20 years ago when four portfolio managers, each with over 20 years’ of experience in Australian Equities, came together to create a unique offering focused on delivering sustainable, competitive returns for investors over the long-term.

Consider this: if you had invested $100,000 in the S&P/ASX 200 index 20 years ago, that investment would be worth over $400,000 today—a fourfold increase. However, had you invested the same amount in Northcape’s Australian Equities strategy, the investment would now be worth over $700,000, a sevenfold increase with a significant impact on retirement outcomes.

As Northcape celebrates two decades managing Australian Equities, here they share three key lessons learned that have helped form the foundation of their success investing in Australian equities.

Lesson 1: Quality Businesses Tend to Outperform in the Long Run

Quality means different things to different people. At Northcape, a quality company is able to sustainably generate returns on capital well above its cost of capital and continue to re-invest at high rates of return. The value of this compound growth is sometimes underestimated by the market, which often displays a shorter-term mindset.

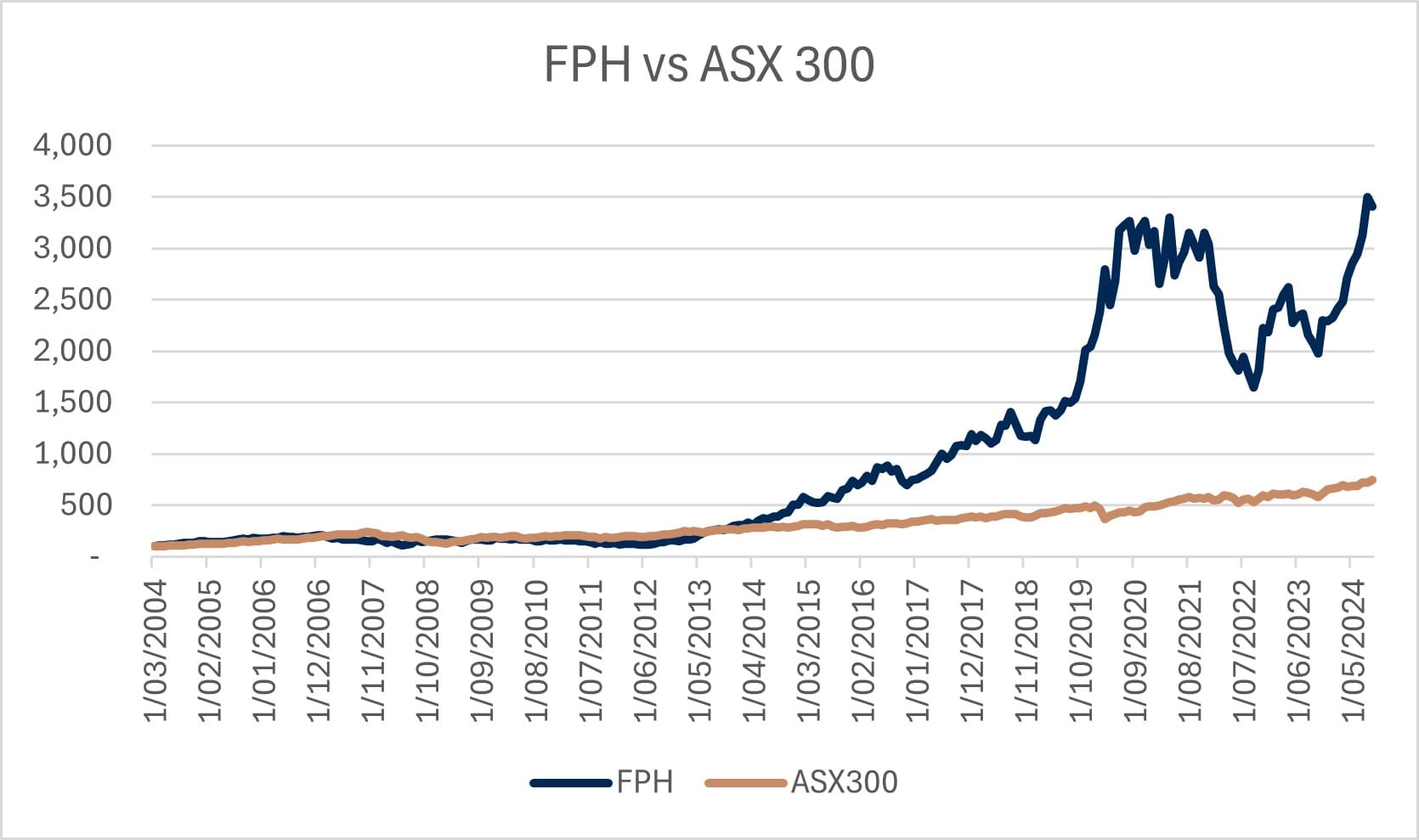

An example is Fisher & Paykel Healthcare (ASX:FPH). It is a company Northcape has held since inception and continues to hold today. FPH makes life-saving hospital equipment to treat patients in respiratory distress, including for conditions such as pneumonia and bronchitis. Its products are also used in post-operative care in hospitals and in the home to treat sleep apnoea.

The company has demonstrated remarkable resilience, achieving a compound annual revenue growth rate of 12% over the 50 years prior to the Covid pandemic as its products were gradually adopted more widely. This growth was supercharged during Covid when FPH sold a decade worth of equipment to hospitals in just 2 years.

Fisher & Paykel’s growth has been driven by its substantial investment in research and development which cements its global industry leadership and creates high barriers to entry. While the market may focus on short-term metrics, we are more interested in the ability of the company to deliver sustained growth over the long term. The performance of the share price is not as steady as the growth of the underlying business, but over time, compound growth in profits has delivered rich rewards to shareholders.

Identifying quality and building our portfolio around a range of resilient businesses like Fisher and Paykel Healthcare will always remain at the core of Northcape’s investment approach.

Source: Bloomberg, October 2024

Lesson 2: Always Avoid Permanent Capital Loss

Markets are regularly swept up in fads, be it for technology stocks, crypto assets, buy-now-pay-later firms, or particular commodities. Fast money in a sector can create its own excitement, further exacerbated by investors’ FOMO (Fear of Missing Out). We think that taking a level-headed approach to these situations can be a major contributor to long-term returns. The key is to think of risk as the possibility of permanent capital loss for clients; not the risk of missing out on a hot investment theme.

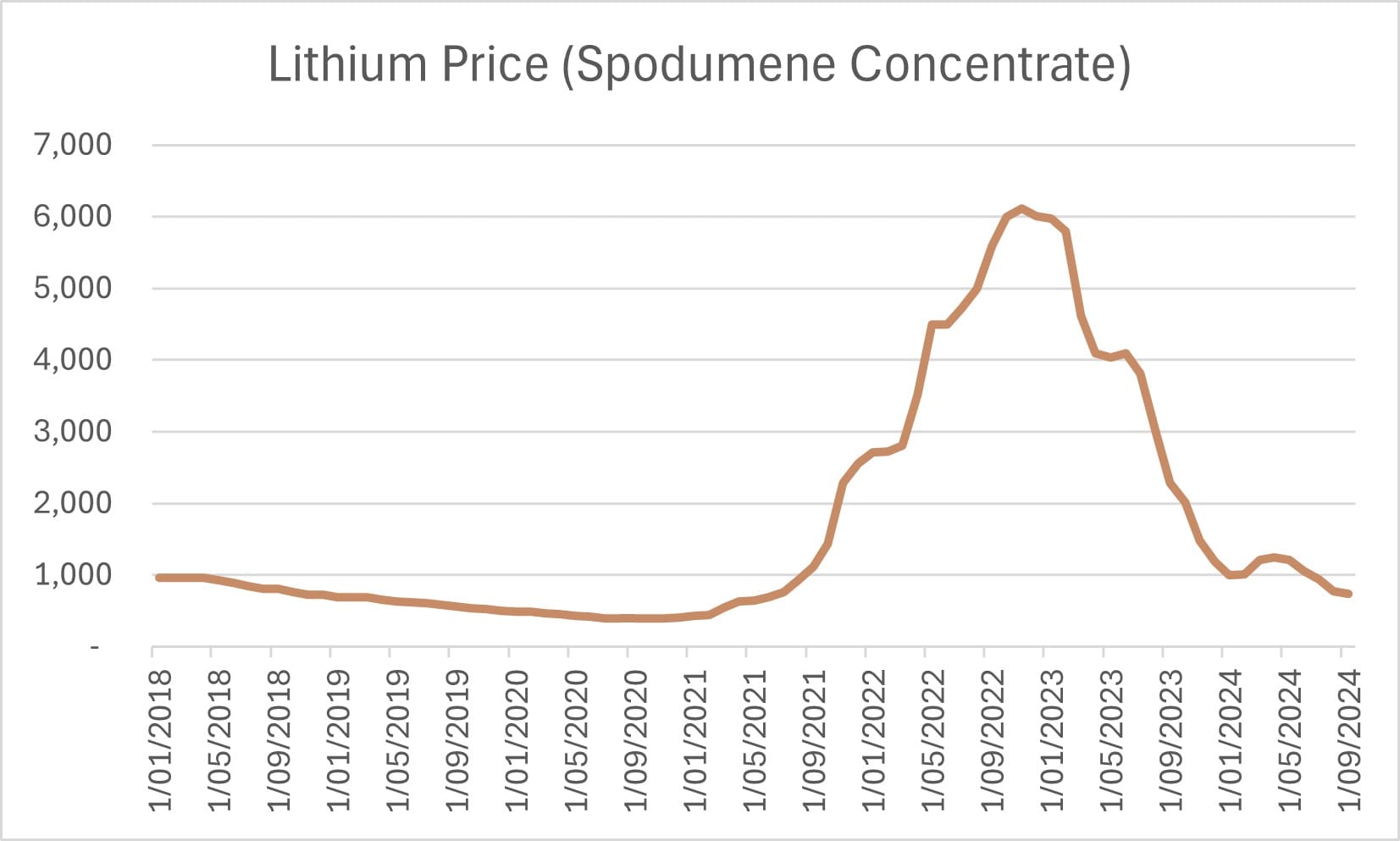

One recent example is the lithium sector. Lithium prices surged sixfold in 2021 and 2022, only to fall dramatically, now below their level at the start of this cycle. The spike in the commodity price incentivised investment in new sources of low-cost supply, and spurred investment in new mining technologies. This has led some lithium stocks to turn from market darling to now be among the worst performers in our market. For example, over the last 12 months Pilbara Minerals (ASX: PLS) is down 35%, IGO Limited (ASX: IGO) is down 60% and Liontown Resources (ASX: LTR) is down 80%.

Source: Bloomberg, October 2024

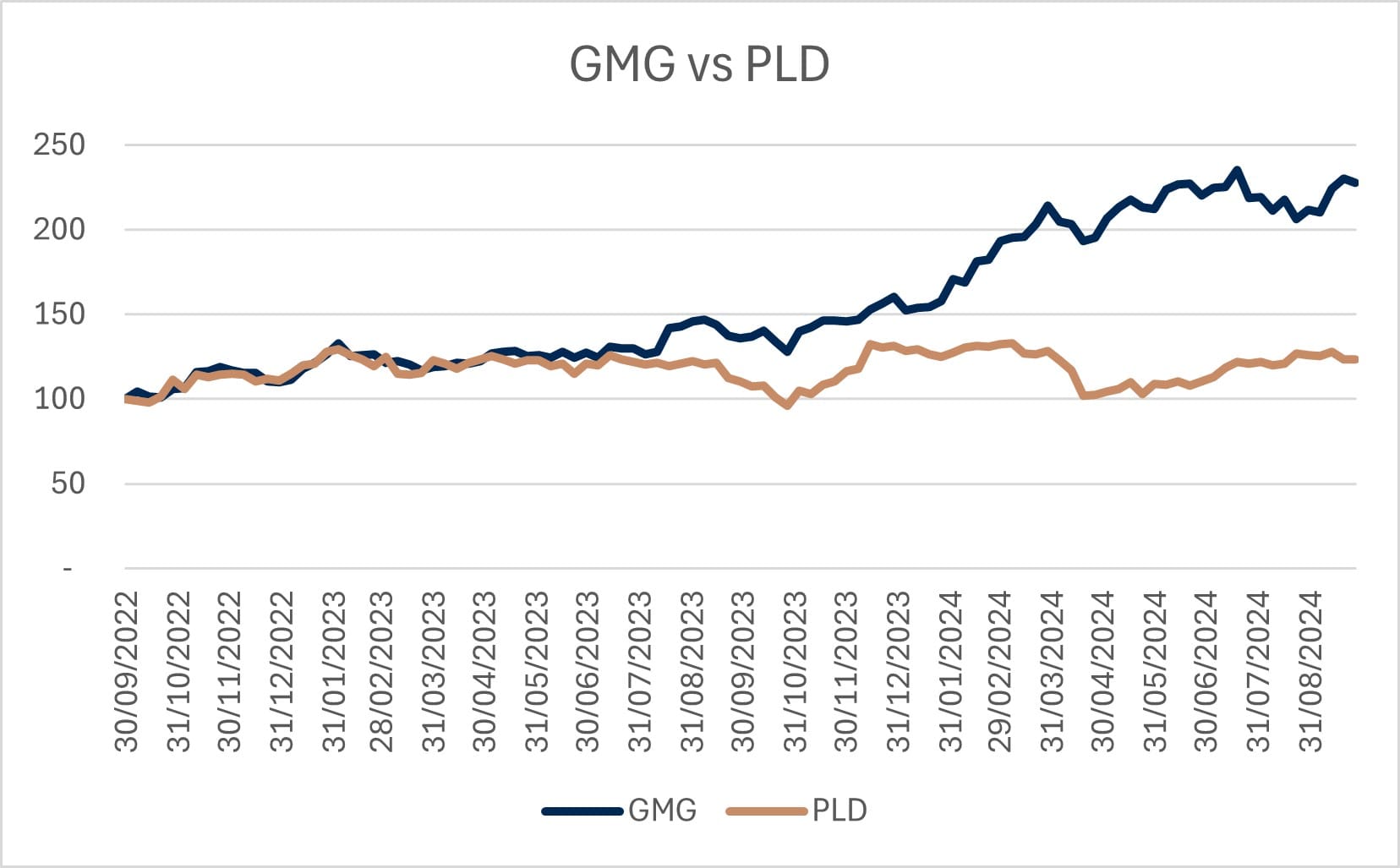

Similar signs of speculative behaviour appear to be emerging in some areas of the Artificial Intelligence (AI) sector today. A lack of AI-themed investment options (no Australian Nvidia!) has driven a rush toward data centre developers such as Goodman Group (ASX: GMG), with its share price up 70% over the last 12 months.

In comparison, the share price of GMG’s US-listed peer Pro Logis (NYSE: PLD) has reflected a more balanced view of industry dynamics and has underperformed GMG by 100% over the last 12 months.

While we see great potential for artificial intelligence, particularly in sectors such as healthcare, we are concerned that the accompanying hype has driven a momentum-fuelled pricing cycle that overstates the prospects for future returns.

Source: IRESS, October 2024

A noticeable change to markets in the last 20 years is the influx of passive, algorithmic and momentum driven strategies. One problem with these approaches is a “herding” effect where rising prices encourage further investment in a circular fashion. In these instances, prices can move well beyond fair value. The risk with this type of momentum-driven, one-way traffic is that it causes sudden and unexpected shifts in the other direction when the herd changes its mind, which can result in significant capital loss. You can think of it like a crowded boat, where the risk of capsizing increases when everyone shifts to one side.

At Northcape, we don’t see risk as missing out on the next hot lithium or AI stock. Rather, we see risk as the possibility of permanent capital loss for clients.

Northcape’s strategy focuses on avoiding businesses with poor quality characteristics, such as over-leveraged balance sheets, misaligned incentives and weak competitive advantages. We take pride in the fact that we have never invested in a company that has gone bankrupt, even during the Global Financial Crisis (GFC).

The table below demonstrates that throughout Northcape’s history our portfolio generally matches the market when the market is rising, while our performance significantly exceeds the index when it is falling.

We achieve this because we do not chase short-term market trends but instead focus on long-term fundamentals. In our view this approach is the most effective way to safeguard our investors from permanent capital loss.

Source: eVestment. Northcape Capital Australian Equities Core Strategy

Lesson 3: Human Judgment Drives Long-Term Outperformance

The range of market participants has grown over time to include more automated strategies and complex risk management systems. One side effect of this trend is that an increasing proportion of share trades are originated by computers – also known as algorithmic trading – with little regard to what the underlying business is worth. Part of our edge in markets is simply the ability to apply human judgement to every investment decision. This approach requires an experienced team and can lead to decisions that run against the direction of the crowd.

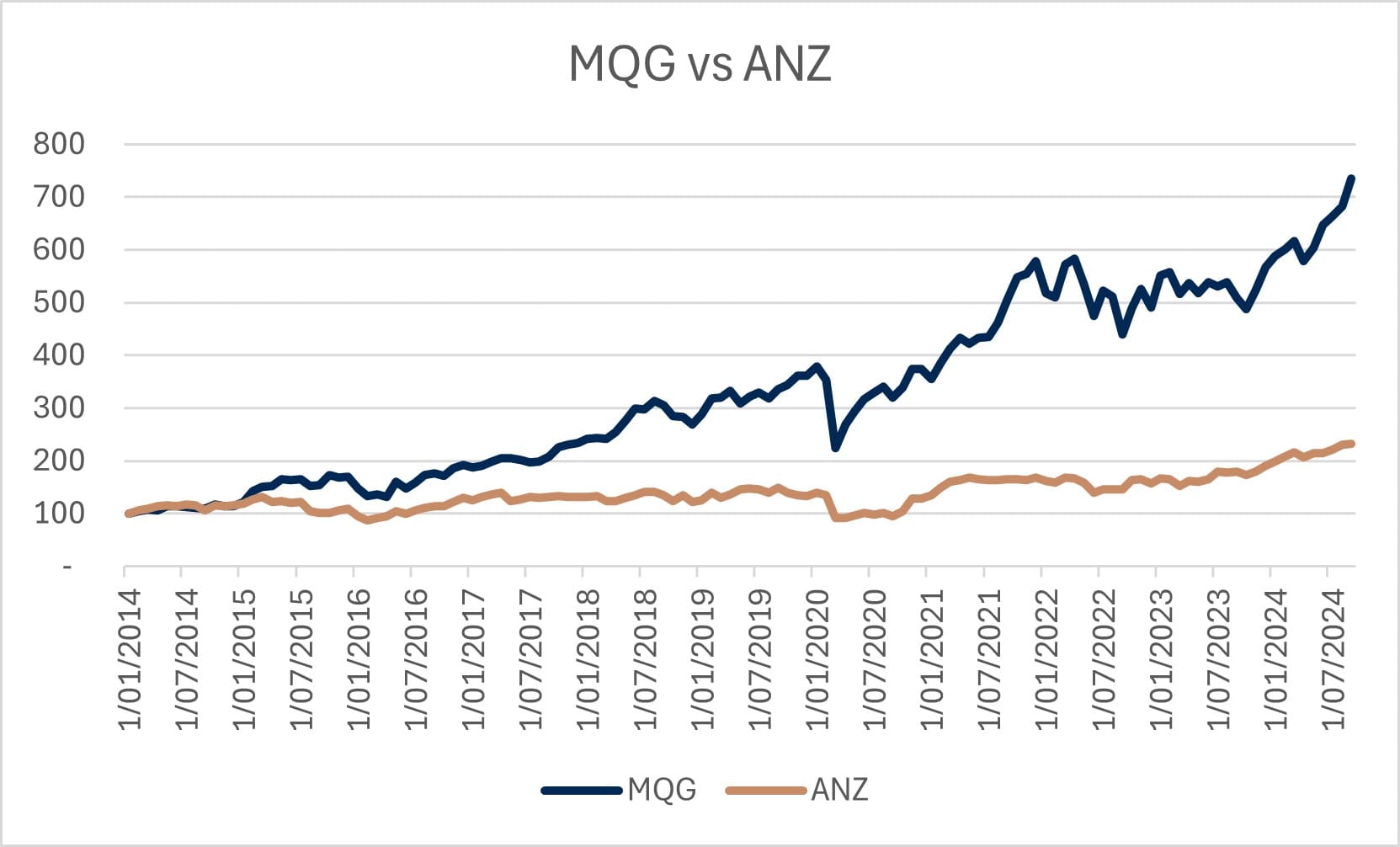

An example is the recent performance of the banking sector. Commonwealth Bank of Australia (ASX:CBA) has seen its share price increase by 20% this year with no changes to earnings expectations. Trading on a Price/Book of 3X, it currently holds the title of the most expensive bank in the developed world. While the momentum in the sector may be attractive to some investors, we are more interested in the outlook for long term profitability. For example, ANZ has also rallied by 20% so far this year but looking back we can see its earnings per share have not grown at all over the last ten years. On this basis, we see more appeal in Macquarie Group (ASX:MQG).

Northcape built a stake in MQG following the Global Financial Crisis (GFC), when global banks faced a highly uncertain future and Macquarie was trading below its tangible book value.

Despite this, we identified:

- A long and consistent track record of earning returns above its cost of capital;

- Management was deploying capital into profitable niches on a global scale; and

- Its earnings mix was moving towards fee-based income streams like investment management, further de-risking the balance sheet.

We have held Macquarie since 2007, maintaining an overweight exposure in preference to the major banks which have similar macroeconomic drivers, but inferior competitive advantages in our view. While the major banks have experienced a significant decline in their Return on Equity (ROE), MQG has sustained an attractive ROE while also delivering much stronger growth. This investment has generated substantial gains for our clients, with the stock rising from $20 a share to over $220 a share, as well as returning over $32 billion in dividends and buybacks over that period.

This underscores the importance of capitalising on market opportunities to acquire high-quality businesses for the long term at favourable prices. Such opportunities require judgment and a disciplined assessment of each company’s merits, something that pure quantitative or passive investment methods cannot provide.

Source: Bloomberg, October 2024

Northcape was founded on the guiding principle that when our clients succeed, we succeed. The key factors behind Northcape’s strong long-term track record in Australian equities have been a focus on finding quality companies, a fundamental approach to risk and capital protection, and applying human judgement throughout the investment process. On the surface these elements may appear simple enough, however applying them consistently and effectively requires discipline and experience.

For more information, please contact us on 1300 927 254 or visit Our Funds.

The information above is for Northcape Capital’s Australian Equities strategy and is published by Warakirri Asset Management Limited ABN 33 057 529 370 (Warakirri) AFSL 246782 and issued by Northcape Capital ABN 53 106 390 247 AFSL 281767 (Northcape) representing Northcape’s view on a number of economic and market topics as at the date of this report. Any economic and market forecasts presented herein is for informational purposes as at the date of this report. There can be no assurance the forecast can be achieved. Furthermore, the information in this publication should only be used as general information and should not be taken as personal financial, economic, legal, accounting, or tax advice or recommendation as it does not take into account an individual’s objectives, personal financial situation or needs. You should form your own opinion on the information, and whether the information is suitable for your (or your clients) individual needs and aims as an investor. While the information in this publication has been prepared with all reasonable care, Warakirri and Northcape do not accept any responsibility or liability for any errors, omissions or misstatements however caused. Portfolio holdings are subject to change. Past performance of the Northcape Australian Equities strategy is not indicative of future performance of the Warakirri Concentrated Australian Equities Fund or the Warakirri Ethical Australian Equities Fund.

![]()